Revolut Joint Account Review: Is It Right for Your Shared Finances?

Managing money with a partner, roommate or family member shouldn't be complicated. Revolut's Joint Account aims to simplify shared finances through its digital-first approach, but is it the right choice for you?

As someone who's analyzed countless financial products, I've taken a deep dive into what Revolut's Joint Account offers, where it falls short, and how it stacks up against competitors. This guide will help you decide if it aligns with your shared financial needs.

What Is Revolut's Joint Account?

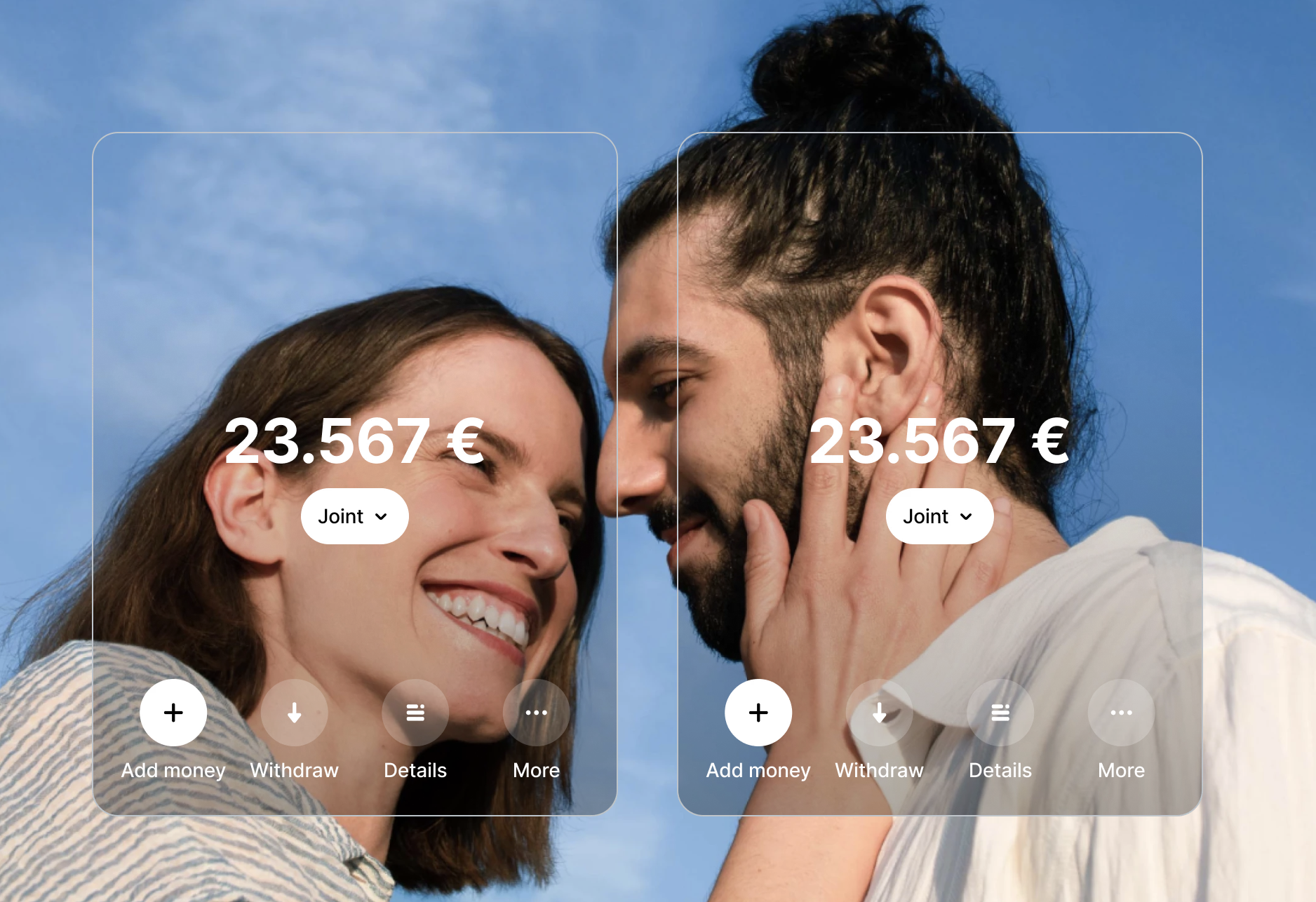

Revolut's Joint Account is a digital account designed specifically for two people to manage shared finances. It functions as a separate account alongside each holder's personal Revolut account, providing a dedicated space for pooling resources and handling common expenses.

The account is available to any two Revolut users who:

- Are 18 years or older

- Have verified personal Revolut accounts

- Live in the same country

- Are registered under the same Revolut legal entity

Unlike some traditional banks, Revolut doesn't limit Joint Accounts to spouses or partners—roommates, family members, and friends can also open one, provided they meet the requirements.

Key Features of Revolut's Joint Account

Equal Access and Control

Both account holders have identical rights to the funds, regardless of who contributed the money. This means either person can:

- Make payments and transfers

- Add money to the account

- Withdraw cash (subject to limits)

- View all transactions and the full account history

This equal control model simplifies management but does require mutual trust, as I'll explain further below.

Individual Cards for Each User

Each account holder receives their own debit card linked to the Joint Account. These cards have distinct details, making it easy to identify who made which purchase in the transaction history. The type of card available (standard, Premium, Metal) depends on the personal subscription plans of the individual users.

Multi-Currency Support

True to Revolut's roots in foreign exchange, the Joint Account supports holding and exchanging over 30 currencies. This is particularly valuable for:

- Couples with different nationalities

- Sharing travel expenses across multiple countries

- Managing international property costs

- Receiving payments in different currencies

Integrated Budgeting with "Pockets"

The Joint Account connects with Revolut's "Pockets" feature, allowing you to create dedicated spaces for specific expenses or savings goals. This helps both users:

- Allocate funds for rent, utilities, or groceries

- Save collectively for shared goals like vacations

- Track spending in different categories

- Maintain financial organization without separate apps

Real-Time Notifications

Both account holders receive instant notifications for all transactions, ensuring complete transparency about how and when money is being spent from the shared account.

Cost and Fee Structure

The basic Revolut Joint Account is free to open and maintain, with no monthly fees. However, various actions may incur charges depending on the personal subscription tiers of the account holders.

| Fee Type | Standard Plan | Premium/Metal/Ultra Plans |

|---|---|---|

| Monthly Account Fee | Free | Free (Joint Account itself has no fee) |

| ATM Withdrawals | £200/€200 or 5 withdrawals free per month, then 2% fee | Higher limits based on personal plan (up to £800/€800 or unlimited) |

| Foreign Exchange | £1,000/€1,000 free per month (Mon-Fri), then 1% fee | Higher or unlimited exchange amounts depending on plan |

| Weekend Exchange Fee | 1% markup on all exchanges (Sat-Sun UTC) | Plus: 0.5% markup Premium/Metal/Ultra: No weekend fee (Effective April 22, 2025) |

| International Transfers | Fee varies by destination and method | Discounts or fee-free allowances based on personal plan |

| Physical Card Delivery | Delivery fee applies | Free standard delivery for premium plans |

It's important to understand that the Joint Account inherits many features and limitations from the personal subscription plans of its holders. For example, users on Premium or Metal plans will enjoy higher fee-free ATM withdrawal limits when using their Joint Account cards.

Recent Fee Update: From April 22, 2025, Revolut is reducing weekend currency exchange fees for paid plans. While Standard customers will continue to pay a 1% markup on weekend exchanges, Plus customers will only pay 0.5%, and Premium, Metal, and Ultra customers will pay no weekend exchange fees at all. This makes the Joint Account even more attractive for frequent travelers with paid subscriptions.

Important Considerations and Limitations

Deposit Protection Differences

One of the most critical aspects to understand about Revolut's Joint Account is how your money is protected:

In the UK:

Funds in standard Revolut accounts (including Joint Accounts) operated by Revolut Ltd are safeguarded, not covered by the Financial Services Compensation Scheme (FSCS). This means your money is held in separate accounts with regulated banks, but doesn't have the same £85,000 government-backed protection that traditional UK banks offer.

In the EEA:

If you're using Revolut Bank UAB (the European entity), your deposits are protected under the Lithuanian Deposit Guarantee Scheme up to €100,000 per depositor.

This distinction is crucial when deciding whether to keep substantial amounts in your Joint Account.

Unilateral Control Structure

Perhaps the most significant consideration is that either account holder can:

- Withdraw the entire balance without the other's permission

- Close the account independently

- Make any transaction without requiring joint authorization

This structure prioritizes convenience but requires absolute trust between both parties. It differs from some traditional joint accounts that may require dual authorization for major actions.

Joint and Several Liability

Both account holders are equally responsible for all activity on the account. This means:

- You can be held liable for transactions made by the other person

- Any fees or negative balances are the responsibility of both parties

- Financial associations are created between both users

No Overdraft Facility

Unlike some competitors, Revolut doesn't offer an overdraft on its Joint Account. While this prevents unexpected debt, it also means you don't have the flexibility of short-term credit when needed.

Limited Cash Handling

As a digital-first platform, Revolut lacks convenient options for depositing cash or cheques. This can be inconvenient if you regularly need to deposit physical money into your shared account.

Customer Support Considerations

Support for the Joint Account is primarily provided through Revolut's in-app chat. While this is convenient for simple issues, it can be frustrating when dealing with more complex problems. Users on paid plans (Premium, Metal, Ultra) receive priority support.

Some users report challenges with account restrictions or freezes, which can be particularly problematic for a shared account that may be used for essential expenses.

Who Should Consider Revolut's Joint Account?

Ideal For:

- Tech-savvy couples or roommates comfortable managing finances exclusively through an app

- International users who frequently deal with multiple currencies

- Existing Revolut customers seeking to add shared financial management

- Light cash users who rarely need to deposit physical money

- EEA residents who benefit from deposit guarantee protection

Less Suitable For:

- UK users prioritizing deposit protection who would prefer FSCS coverage

- Those who value traditional banking features like overdrafts or branch access

- People who prefer phone support over chat-based assistance

- Heavy cash handlers who regularly need to deposit physical money

- Users with complex financial arrangements who need more than two people on an account

How to Open a Revolut Joint Account

Setting up a Joint Account is straightforward and entirely digital:

- Both individuals must have active personal Revolut accounts

- One person initiates the process by selecting "Accounts" → "Add new" → "Joint Account"

- They invite the second person (who must already be a contact in their Revolut app)

- The invited person accepts the invitation in their app

- Revolut conducts any necessary additional verification

- Once approved, both users can add funds and start using the account

The Bottom Line

Revolut's Joint Account offers a modern, convenient solution for managing shared finances, particularly for internationally active, digitally fluent users. Its multi-currency capabilities and integrated budgeting tools are standout features, especially for those already in the Revolut ecosystem.

However, the lack of FSCS protection for UK users, unilateral control structure, and limitations around cash handling and customer support mean it's not the ideal choice for everyone. Before committing, carefully consider your priorities around deposit protection, account control, and the specific features you need from a shared account.

For many digital-first users, particularly those with international financial needs, the convenience and functionality will outweigh the drawbacks. For others, alternatives like Monzo or Starling in the UK, or N26 in Europe, might provide a better balance of features and protections.

Try our Broker Match tool to find the perfect banking solution for your specific needs, or explore our full range of banking reviews.

For a broader look at Revolut's banking and investing features, including how it compares to other platforms, read our in-depth Revolut review.

FAQs About Revolut's Joint Account

Is my money safe in a Revolut Joint Account?

In the UK, funds are safeguarded (held separately from Revolut's own money) but not covered by the FSCS. In the EEA, deposits are protected up to €100,000 under the Lithuanian Deposit Guarantee Scheme. This difference in protection is important to consider when deciding how much to keep in your account.

Can either account holder withdraw all the money?

Yes, either person can withdraw the entire balance without the other's permission. This makes trust between account holders essential.

What happens if one account holder wants to close the account?

If the balance is zero, either holder can request closure without the other's consent. Revolut will notify the other party but can act on just one person's request.

Can I have multiple Joint Accounts with different people?

No, Revolut limits users to being part of only one Joint Account at a time.

How does a Revolut Joint Account compare to traditional bank joint accounts?

Unlike some traditional joint accounts, Revolut doesn't offer overdrafts, has limited cash deposit options, and operates with a unilateral control structure where either person can perform any action independently. However, it offers stronger multi-currency capabilities and a more modern digital experience.

Can we upgrade our Joint Account to Premium or Metal?

The Joint Account itself doesn't have subscription tiers, but it inherits features and limits based on the personal subscription plans of its holders. Upgrading your personal account will enhance your experience with the Joint Account.

What happens to the Joint Account if one person's personal account is restricted?

If either holder's personal account becomes restricted, this may affect their ability to use the Joint Account. In cases of suspected fraud or violations, Revolut may restrict the Joint Account as well.